Following the footsteps of RBI, SEBI and IRDAI, PFRDA on 06 October 2020, has decided to allow registered intermediaries with PFRDA to onboard, deboard or provide essential pension services to subscribers via Video based Customer Identification Process (VCIP). The regulator asserts that this will greatly benefit both the intermediaries and the subscribers from faster verification, quicker turnaround and most frugally removes the need for subscribers to be physically present before nodal officers (POPs) for verification. VCIP will also benefit the POPs to have an online only presence and provide services to customers and carry out regulatory due diligence from anywhere in the country.

What is video KYC (VCIP)

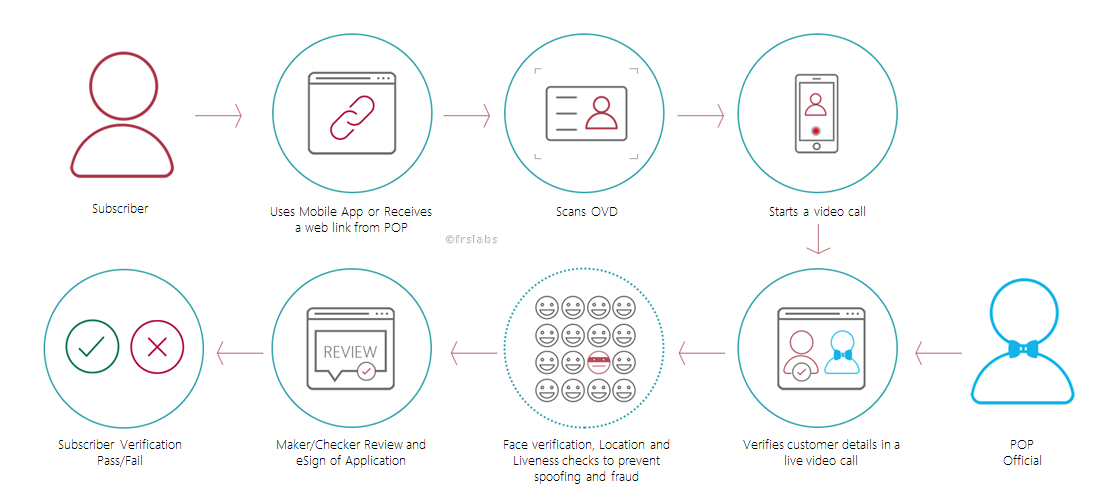

Video KYC is the process of verifying a subscriber through a live recorded video call. The entire process must conform to the regulatory norms set by PFRDA as described below.

Mobile application based VCIP: This refers to allowing the subscribers to complete the verification process using a mobile application provided by the POPs.

- POPs should provide their own mobile application to subscribers for undertaking VCIP.

- The mobile application should facilitate the subscriber taking photograph, scanning or uploading of OVDs, capturing of signature and carrying out live Video verification with the POP official.

- The VCIP can be carried out by an authorised official of the POP and cannot be done by a third party (i.e. VCIP cannot be outsourced to third parties by POPs).

- The official conducting the VCIP shall ensure that the questions and the sequence are varied in order to establish that the audiovisual interactions are not pre-recorded.

- Prior to establishing the video call, the POPs must ensure that the customer doing the VCIP is physically present in India.

- POPs shall ensure that the process is seamless, real-time, secured and end-to-end encrypted audiovisual communication with the customer undergoing

- The POP official ensures that sufficient liveness checks are carried out to prevent spoofing and fraudulent manipulations.

- The Video KYC software to be deployed undergoes security and audit validation to ensure security, robustness and end to end encryption of the Application.

- POPs should ensure that the quality of the video is adequate to establish identification of the customer beyond doubt.

- As a mandatory step, POPs must carry out instant bank account verification through penny drop.

- The POPs should generate the soft copies of CSRF (Subscriber registration form) – using the photograph, OVD and signature uploaded – and share it with CRA and subscribers following the completion of VCIP at the time of onboarding.

- During exit, the withdrawal document along with the KYC needs to be uploaded by the subscriber and verified using VCIP for the purpose of issuing annuity by Annuity Service Providers.

Non-Mobile application based VCIP: This refers to POPs carrying out VCIP through a web interface with the subscriber. This can also refer to the POP initiating a VCIP request through an SMS or Email which the subscriber can accept with consent to complete the VCIP verification with the POP official.

- The Video KYC call must be completed by a trained official with informed consent of the subscriber.

- The entire activity log and the metadata captured during the video kyc along with the credentials of the official performing the video kyc and timestamps shall be preserved.

- The VCIP can only be carried out in a live and undisturbed environment and that the subscribers face must be fully visible during the VCIP.

- The official shall ensure that the questions and the sequence are random in order to establish that the audiovisual interactions are not spoofed.

- POPs to ensure that the photograph in the KYC document/CSRF/Exit form (as the case may be for the services opted by the subscriber) matches with the live face obtained during the VCIP.

- The video session with the subscriber should originate from the domain of the POPs and not originate from a third-party system.

- As a mandatory step, POPs must carry out instant bank account verification through penny drop.

- The POPs should generate the soft copies of CSRF (Subscriber registration form) – using the photograph, OVD and signature uploaded – and share it with CRA and subscribers following the completion of VCIP at the time of onboarding.

- During exit, the withdrawal document along with the KYC needs to be uploaded by the subscriber and verified using VCIP for the purpose of issuing annuity by Annuity Service Providers.

Further, as part of circular point 3 (v), the regulator has suggested that OTP/eSign based authentication (i.e. Aadhaar eSign) be part of the VCIP process to make it completely paperless. This would mean that if, at point a signature is needed of the subscriber, the same be done using Aadhaar OTP based eSign.

How we can help

FRSLABS, an ISO 9001/27001/eSign ASP(NSDL) certified company, provides an award-winning customer onboarding platform that readily conforms to PFRDA’s VCIP steps. Intermediaries can use our white labelled mobile application and web application without the need for any capital expenses or integration and can quickly roll out Video KYC solution for your subscribers with the Intermediaries’ own branding. Our solution comes with OVD Capture, OVD Verification, Photo capture, Liveness checks, Penny Drop verification, eSign, end to end encryption, geo-location check, and all of the regulatory requirements to comply with VCIP.

Download a PFRDA VCIP checklist from here>